A quick guide to the basics of RTP

I would like to start by stating that the purpose of this document is not to get an in-depth breakdown of the RTP System and how its intricacies operate, but instead to create a foundation of knowledge around this new Payment System.

Payments in the United States have traditionally lagged with regard to innovation. That all changed in November 2017 when The Clearing House (TCH) launched the RTP System. Up until that point, the only other Real-Time Gross Settlement (RTGS) system that we had in the United States was the Fedwire System. Unlike its net settlement counterpart, ACH, RTGS systems behave differently because the funds sent via these systems settle in real-time versus in batches during set periods throughout the day.

The RTP System has now existed for just over three years and since its creation, a lot of lessons have been learned and enhancements to the network have been made.

What is the RTP System?

In short, the RTP System is a new innovative system operated by TCH that allows participants of the network to send and receive funds instantly 24/7/365 and send other additional message types that enhance the overall payer and payee experience. Below is a list of a few of the features that I believe truly make the RTP System stand out.

- 24/7/365 functionality: The RTP System is always on unlike other payment systems (ACH/Wire).

- Instant settlement and transfers: RTP Payments are settled instantly into the recipient’s account upon their bank (FI Participant) receiving the payment via the RTP System. This is accomplished thanks to a partnership between TCH and the Federal Reserve Bank of New York (FRBNY) — I’ll discuss how it works in more detail later on.

- Irrevocability: RTP Payments operate similarly to wires with respect to payment finality. Once funds are sent to the system, they cannot be revoked or recalled by the Payer. This has pros for both the sender and the receiver in every transaction. It is beneficial to the receiver because once they receive the funds in their account, they are good and usable. The payer receives payment certainty benefits because once the recipient receives these funds, the payer receives notice of payment confirmation almost immediately.

- Cash Management: Access to a true 24/7/365 RTGS system allows the users of the network to gain control over their cash management like never before. Businesses operate around the clock, but until now, their payments haven’t. Thanks to the introduction of the RTP System, payments can now operate at the same pace that real life does.

- Ubiquity and convenience: One of the biggest hurdles that innovation faces is adoption but thanks to TCH’s wide network of Participant Banks, adoption of the system has been steadily increasing and now reaches over 56% of all United States demand deposit accounts (DDAs).

What is RTP used for?

RTP Transactions can serve a multitude of use cases within the B2B, B2C, P2P, and C2B space. Creative use cases are being crafted regularly and are helping solve niche problems that exist amongst businesses and consumers.

Some of the more common use cases that have been showcased by TCH on their website are the following:

B2B

- A small business paying an urgent invoice to receive goods or services

- Restaurateur paying for farm-fresh produce from the local farmer

B2C

- Utility company requesting payment for services from a business or consumer

- Small business paying temporary employee salaries or tips on an ad hoc basis

- Retail bank distributing personal loan proceeds to a dealership on behalf of a consumer buying a new car

- Insurance company determining a settlement amount for a claim and immediately providing funds to the policyholder

- Large corporation paying employees for travel expenses

- Large corporation running payroll for its employees on for early wage access

P2P

- Roommates splitting monthly rent and utility payments

- Sending a friend/spouse/loved one emergency funds

C2B

- The busy working individual paying for general services such as gardening, cleaning, or childcare

- A day trader sending real-time money transfers to their investment account

Source: https://www.theclearinghouse.org/payment-systems/rtp

How does the RTP System work?

Before diving into the RTP System and how its different message types operate I’ve included a dictionary to help describe the vocabulary that is typically used with the RTP System:

Payer: The Person or company that wishes to send a payment.

Payer’s FI: The financial institution (FI) whose customer wishes to send a payment.

The RTP System: A network for routing and settling payments between participating FIs.

Payee’s FI: The FI that receives the payment for its customer’s account.

Payee: The person or company that receives the payment.

Participant: A depository institution that has entered into a Participant Agreement and Indemnity with TCH.

Credit Transfer: The basic multi-purpose Payment Message used for multiple use cases, including remittance information.

Payment: A transfer of value from a Sender to a Receiver through the RTP System pursuant to a Payment Message

Instruction: Any Message that initiates a new exchange of Payment or Payment-related information between two Participants in the RTP System or between the Participant and the RTP System. (Credit Transfer, Request for Payment, Request for Information, Remittance Advice, etc.)

Leg: A transmission from an FI to the RTP System or the RTP System to an FI. It should be noted that either FI may initiate an RTP Instruction

Message: A transmission of an Instruction or of a Response from one FI to another FI through the RTP System

Transaction: A full round-trip of an Instruction and Response Messages. All Payment Transactions have 5 legs including the Payee’s FI Confirmation Leg. Payment-related Transactions have 4 legs and RTP Control Messages have 2 legs.

Event: An exchange of related transactions between two FIs through the RTP System that constitutes a complete conversation. This could include one or more Transactions.

Source: https://www.theclearinghouse.org/payment-systems/rtp

Credit Transfer Transaction

This Transaction is the basic multi-purpose Payment Message used for multiple use cases, including remittance information. The transaction limit for an RTP Credit Transfer Transaction is $100,000 USD and the RTP System is only eligible for use domestically. Additionally, the RTP System functions as a credit-only payment system. This means that funds can only be pushed out of accounts and not debited, or pulled in, from other people’s or businesses’ bank accounts. There is a way to use a different transaction type called a Request for Payment to receive funds, but it still requires a Credit Transfer Transaction as a response from the Payer to the Payee and behaves more like an electronic invoice than a true debit.

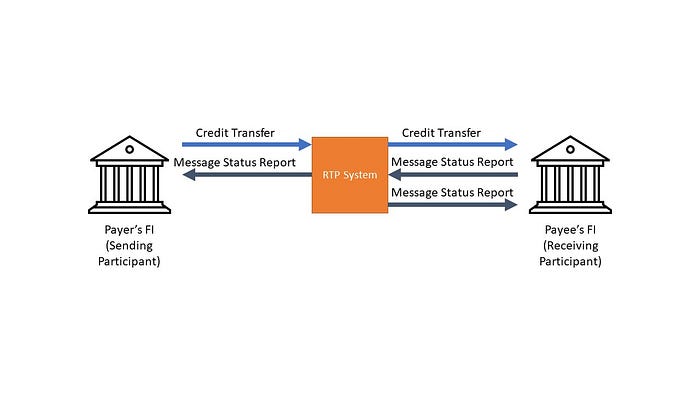

The simple diagram below demonstrates how a Credit Transfer functions between FIs. I’ve purposely left out the Payer and Payee to keep things simple and only show how the System operates across banks. In a true Credit Transfer Transaction, the Payer would send Payment Instructions to its FI (via an API or UI) and the Payer’s FI would then perform some type of verification and approval process prior to sending the first leg of the Credit Transfer Transaction to the Network.

The Process

- The Payer’s FI sends the Credit Transfer Message to the RTP System.

- The Payee’s FI receives the Credit Transfer Message.

- Payee’s FI validates the Message and then sends a Message Status Report. This message will indicate whether the FI accepted or rejected the Credit Transfer Message.

- The Payer’s FI receives the Message Status Report from TCH with a status update of “accept”, “reject”, or “accept without posting.” (Note — don’t worry about the last one yet I’ll explain what this means another time but just know that it exists as a possible status)

- The final leg of the Credit Transfer Transaction is the final Message Status Report that is sent from the RTP System called a “Message Receiver Confirmation.” This final message notifies the Payee’s FI that the response was received and the transaction settled. After this occurs the Payee’s FI makes the Payment available to Payee.

The above process only shows the messaging portion for Credit Transfer Transactions; however, there is a lot more that happens in the background. After all, apart from the messages, the core component of this system is to instantly transfer funds (i.e. move money from one account to another account… instantly). So, how does it actually work?

The image below highlights what the process looks like when the fund flow portion of the RTP Credit Transfer Transaction is added to the mix. Notice that there is now an additional bank icon. This is the Federal Reserve Bank of New York (FRBNY). In order for the RTP System to function properly, there needs to be a Prefunded Balance Account that lives outside of the Payer’s FI and Payee’s FI relationship. This Account is jointly owned by all of the Participants on the network; however, TCH is the sole agent of the Account. This account’s purpose is to hold all of the pre-funded balances in order to ensure that all of the Credit Transfer Transactions being sent are good funds.

Whenever a Credit Transfer Transaction is completed, the RTP System will decrease and increase the Payer FI’s and Payee FI’s pre-funded balances, respectively. Whenever a Participant’s Prefunded Balance goes below the value of the Credit Transfer Transaction they are trying to send, the RTP System will immediately reject it until the Participant pre-funds their balance again via Fedwire. (note — there is another way for a Participant to pre-fund the account if their balance drops too low that involves an FI-to-FI RTP Credit Transfer but that is more complex than the intended level of this guide).

The More Accurate Process

- The Payer’s FI sends the Credit Transfer Message to the RTP System.

- The Payee’s FI receives the Credit Transfer Message.

- Payee’s FI validates the Message and then sends a Message Status Report. This message will indicate whether the FI accepted or rejected the Credit Transfer Message.

- Once the RTP System receives the “accepted” Response Message, the System settles the transaction by decreasing and increasing the Payer’s FI and Payee’s FI’s Current Prefunded Positions and then sends the Payer’s FI the Response Message.

- The Payer’s FI receives the Message Status Report from the RTP System with a status update of “accept”, “reject”, or “accept without posting.” (Note for this example with settled funds the message received would be “accept”).

- The final leg of the Credit Transfer Transaction is the final Message Status Report that is sent from the RTP System called a “Message Receiver Confirmation.” This final message notifies the Payee’s FI that the response was received and the transaction settled. After this occurs the Payee’s FI makes the Payment available to Payee.

Key Takeaways

After reading this guide you should now have a basic understanding of what the RTP System is, what it is used for, and how it functions with a Credit Transfer Transaction. There are many other message types that can be used such as Request for Payment, Request for Information, Remittance Advice, and more.

What is the RTP System?

A network for routing and settling payments between FIs on the network.

What is it used for?

The RTP System can be used for various use cases ranging from B2B, B2C, P2P, and C2B. Remember that transactions cannot exceed $100,000 USD and the System is only operational for domestic payments. Finally, you can’t pull funds from people or businesses’ accounts, you can only push money out.

How does a Credit Transfer Transaction work?

- Payer’s FI sends Credit Transfer Message to the RTP System

- RTP System sends Credit Transfer Message to the Payee’s FI

- Payee’s FI responds with Message Status Report

- RTP System rebalances Prefunded Positions at FRBNY

- RTP System sends Message Status Report to Payer’s FI

- RTP System sends Message Status Report to Payee’s FI

More to come on RTP

Hopefully, this post was a helpful quick guide for learning some of the foundational information about RTP. I’m going to write more posts ranging from other quick reference guides to more complex documents as well as best practices that I have learned through my journey both as a product manager on the banking side and as an operator on the fintech side. My intentions are to create supplemental resources for people interested in learning more about RTP as well as startups and businesses thinking about using these in their daily operations. Some topics to expect in the future:

- The different RTP Messages and their uses

- RTP Transactions and Events — more complex payment flows

- Things to know before launching a faster payments startup

Feel free to tweet me @StartupSebas